December general market comments

Dance across the floor – Jimmy “Bo” Horne, 1978

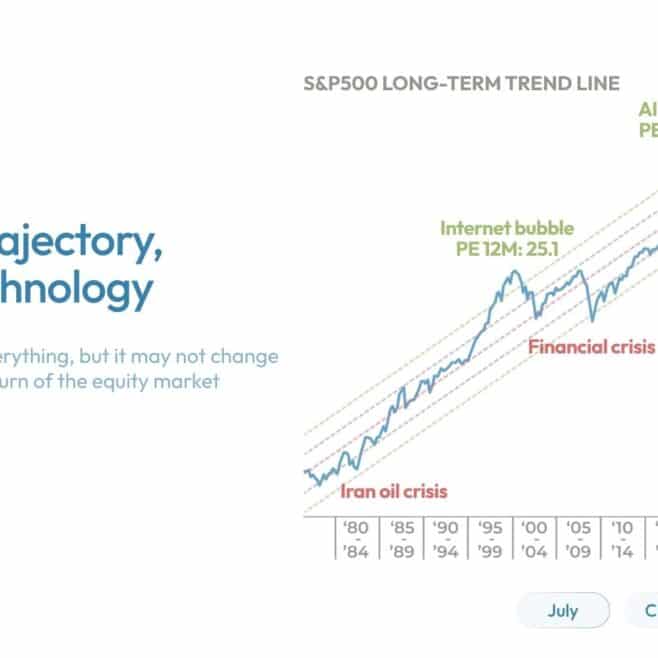

When Jimmy “Bo” Horne wrote this song in 1978, the “floor” still prevailed on the New York Stock Exchange; this was the place where most of the equity transactions were done, with traders and brokers actively buying and selling stocks. A decisively good year for equities traditionally ended with a festive atmosphere on the pit. Electronic trading has gradually started to supplant physical trading in the 80s, and has now almost entirely replaced it. With 2024 marking a very rare back-to-back 20% + yearly return for the S&P500, we can imagine that traders and brokers would have danced across the floor on the 31st of December, especially that, despite Covid, interest rates, inflation and geopolitics, the index has delivered a whopping 186% price performance since 2014.

Things could even have been better if December 2024 had not been a poor month for equities in general; the US economy is still defying the Cassandras, marking a sharp contrast with most regions. Fed’s ample easing expectations are being rattled down, with higher yields and a much stronger USD as a consequence. To wit, the US 10 year yield rose by 40 bps (+28 bps for the Bund), and the broad dollar index soared 2.6% (underneath the surface, the Euro was down 2.16%, but the Yen tanked 5.07%). WTI caught up 5.47% and ends the year flattish, Gold receded a tad (-0.7%, but still +27.2% for the year) and credit was barely down in an overall pretty positive year (+7.2% for the Itraxx Crossover in 2024).

When it comes to equities, very often does December confirm, and sometimes amplify, the general trends observed during the previous 11 month of any given year. 2024 was no exception, as, even if the market struggled contrarily to the rest of the year, style and sectors stubbornly maintained their trajectory. The nascent reversal triggered by Mr Trump’s win (the “Trump trade”) entirely faded and market polarization came back in force. Growth smashed Value with the Nasdaq up 0.4% versus -2.5% for the S&P500, but more striking is the performance gap between the MSCI World Growth and the MSCI World Value: +0.4% for the former and -5.8% for the latter in December, and +25.1% versus +9% in 2024, an incredible 1610 bps difference! Needless to say that winning Growth stocks, and among them the Magnificent-7 (or possibly the “Heavyw-8” with the addition of Broadcom), are in the US, which explains the vast outperformance from US equities versus all other markets so far.

That’s it for this month’s Market Comments, stay tuned, markets never skip a beat.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS PARTNERS SA provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data or other financial instruments referred to in this general comment. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: