July general market comments

“Electric Avenue” – Eddy Grant, 1982.

The world is charging down “Electric Avenue,” fueled by a surging demand for electrification. Artificial intelligence and sprawling data centers crave vast power to process and store the digital revolution, lighting up the global grid. Emerging markets are plugging into this current, electrifying homes and industries to leap into modernity. Electric vehicles are rolling off the line, their batteries humming with energy, reshaping transportation worldwide. HVAC systems, vital for comfort in a warming climate, draw more juice to cool and heat our spaces. From factories to cities, the rhythm of electrification beats stronger, echoing Eddy Grant’s call to “move to the left, move to the right” with sustainable innovation. Renewable sources like solar and wind are stepping up, yet the strain on infrastructure grows.

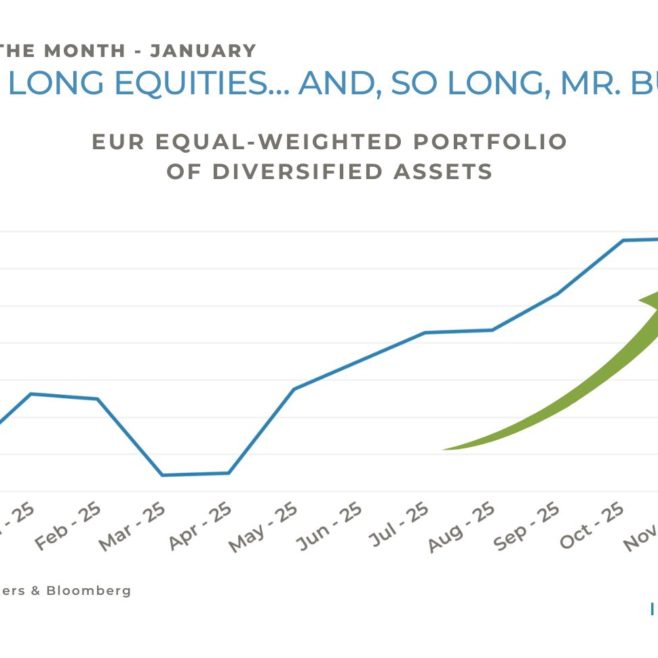

Yes, the world turns even more electric, as markets do: in a month of quarterly earnings reports, equities fared quite well and greed was felt all along the way. Safe havens like Gold or long term Government bonds were weak (first down month for Gold in 2025, but a shallow negative 40 bps), while one of the most speculative assets, Bitcoin, soared by 8.3%.

The MSCI World added 1.2%, the S&P 500 2.2%, the Stoxx 600 0.9%, and Emerging Markets 1.7%; Growth regained the lead with a +2.1% advance for the MSCI World Growth (+0.3% for Value), while Defensives in general had a poor month, contrarily to Cyclicals, among which Electricity and Energy Efficiency players shone.

The dollar showed some signs of rebellion, rising 2.9% and 4.5% respectively versus the Euro and the Yen, and Credit posted another solid return (+1.1% for the Itraxx Crossover, which is now up 5.1% year to date).

With tariffs heavily impacting currency markets and earnings and guidance driving equites, we witness wild moves all over the place; it is remarkable, for example, that the S&P 500 has caught up with the Stoxx 600 on a year to date basis (not adjusted by foreign exchange rates), thanks to the powering ahead of the usual suspects, namely big tech stocks that are absent from European markets.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS PARTNERS SA provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data or other financial instruments referred to in this general comment. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: