August general market comments

“(Everybody Wanna Get Rich) Rite Away” – Dr John, 1974.

As August 2025 draws to a close, the financial markets are dancing to the frenetic beat of Dr. John’s “(Everybody Wanna Get Rich) Rite Away,” a funky anthem that captures the universal itch for quick wealth. This month, that rhythm pulsed through global equities, with the Shanghai Composite Index surging nearly 20% from its early August low, adding almost a trillion dollars in market value despite China’s economic headwinds, tariffs, a property slump and persistent deflation.

The S&P 500, meanwhile, pushed past 6,400, riding a 60%+ rally since October 2022, fueled by AI hype and Fed rate cut optimism. It’s a bull market on steroids, but the lyrics’ warning – “If you wanna be rich and you wanna be wealthy, I believe I’d rather be poor and healthy”- echo a growing unease. The rush to riches is evident in China’s 2.1 trillion yuan in margin debt, nearing the 2015 bubble peak and US tech stocks’ outsized gains, reminiscent of the dot-com frenzy. Volatility spiked early in the month, with the VIX jumping to 30 on August 5, reflecting investor jitters beneath the rally’s surface.

Central banks and policymakers tout stimulus and soft landings, but the relative disconnect from fundamentals, flat consumer prices in China, slowing US earnings growth -suggests a speculative bubble inflating alongside this bull run. Dr. John’s swampy groove reminds us that chasing instant wealth can lead to a “racka tacka tacka rum-dum game,” where very few win if sentiment sours. Caution, not just celebration, is the order of the day as September looms.

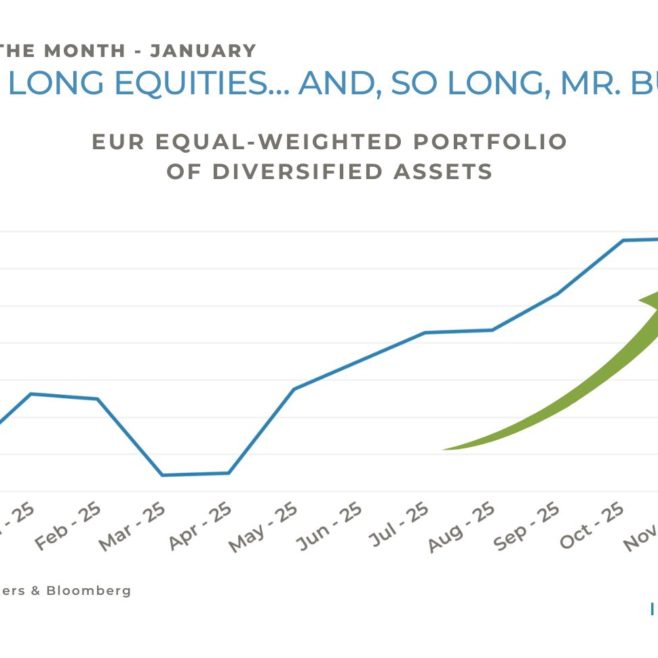

In a month marked by the end of the Q2 earnings season, which was good but not upbeat, the MSCI World added 2.5%, the S&P 500 1.9% and the MSCI Europe 0.7%. Big advances were recorded in Japan (+4.5%) and China (+10.3%). With looming rate cuts from the Fed, the dollar lost 2.3% versus the euro, US 10 year yields hovered 15 bps lower, and Gold, Bitcoin and Oil soared 4.8%, 8.3% and 6.4% respectively. The renewed political uncertainties linked to France’s very poor budget and debt situation probably limited the euro’s rise, but no panic visible so far: year to date, French 10 year yield is up 33 bps, similar to Germany (+35 bps). Still, France borrows more expensively than Greece now, which was unthinkable some years ago.

Credit fared well, but spreads are ultra-low all across fixed-income credit instruments, leaving little room for further tightening.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS PARTNERS SA provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data or other financial instruments referred to in this general comment. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: