Quarterly Investment Review – Q3 2023

Quarterly Investment Review – Q3 2023

“The market is still dominated by investors that either will not (index funds), cannot (untrained novice investors) or chose to not (valuation indifferent prof. investors) have valuation as a cornerstone of their investment process.” David Einhorn

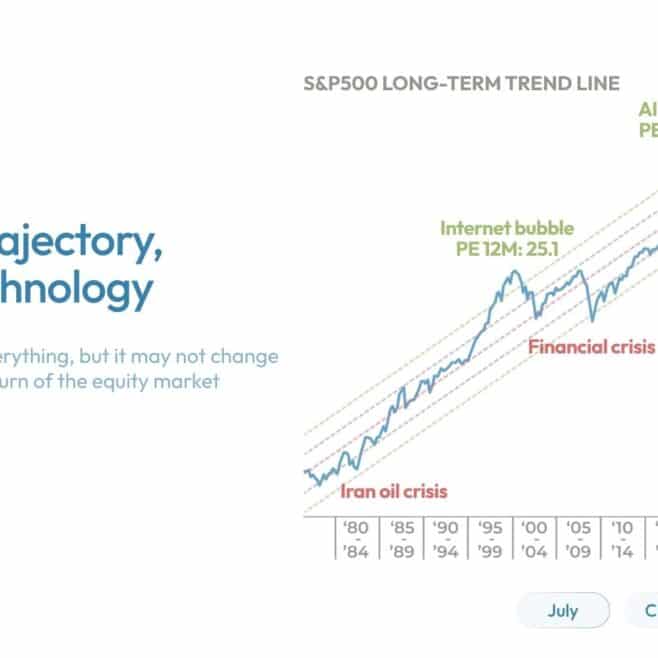

After the turbulence in the Spring when several banks collapsed, including Credit Suisse, equity markets recovered steadily helped by easier liquidity conditions, resilient economic data, a perceived peak in inflation and reasonable profit growth. By the end of September, the S&P500 was up 11% and the MSCI World Index was up 9.6%. However, these returns are misleading. The strong performance has been generated almost entirely by seven stocks (Apple, Microsoft, Alphabet, Amazon, Tesla, Meta and Nvidia). These stocks are up on average 91% and excluding them the indices are only modestly positive. The size of these companies is astonishing. Collectively their market cap equals about 40% of US GDP or 10% of global GDP. Apple and Microsoft’s market cap would place them in the top ten of the world’s largest countries by GDP. For example, Apple’s market cap reached $3 trillion, comparable to the GDP of India, the UK or France. Nonetheless with the market recovering so strongly since the Spring risk assets are now more sensitive to downside surprises and more caution is warranted. In particular, if the view that inflation is settling back down to pre-Covid levels is undermined, then both bond and equity markets would react poorly. Inflation has fallen due to lower commodity prices and supply chains stabilising, but a further fall is more likely to be caused by lower demand thus eroding company profits. At the end of the quarter the oil price started rising, and along with some large wage increase settlements, inflation may stay higher for longer. If this continues there is likely to be more pressure on the highly valued areas in the market, including the mega cap stocks.

Since early 2022 the world has undergone one of the sharpest interest rate rises in history. Following a long period of near zero rates, they have risen, in the case of the US, by 5.25% since March last year. Higher rates raise several concerns. The lagged effects of significant interest rate rises will burden the economy because of the higher financing costs. Many mortgage holders, businesses and investment funds took advantage of the cheap financing available when interest rates were low, and are now facing the reality of much higher rates as their loans are renewed.

Click here to download the full document.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS Partners provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data, quotes, research notes or other financial instrument referred to in this document. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: