Why Cat Bonds Are a Powerful Fixed Income Diversifier in 2026

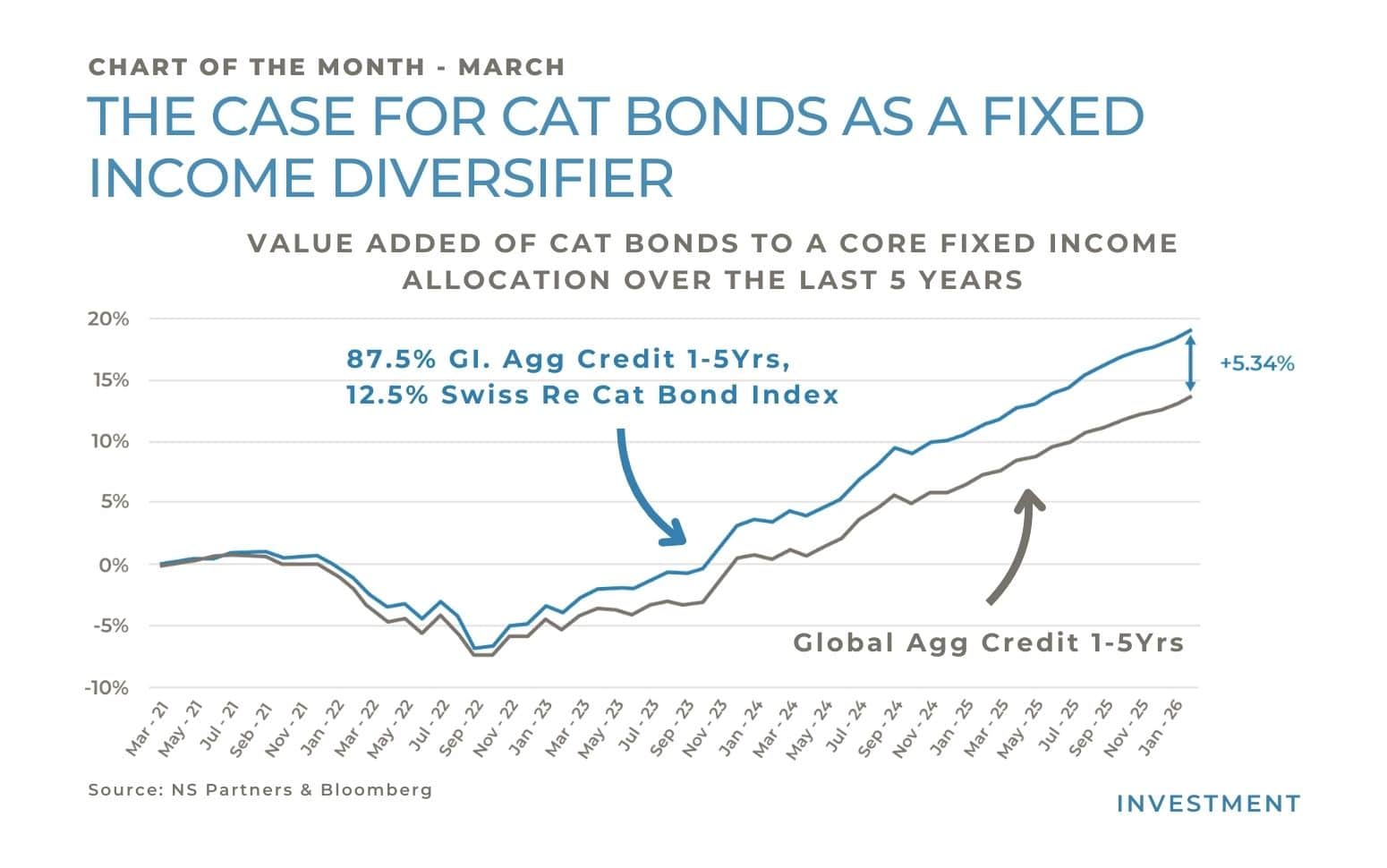

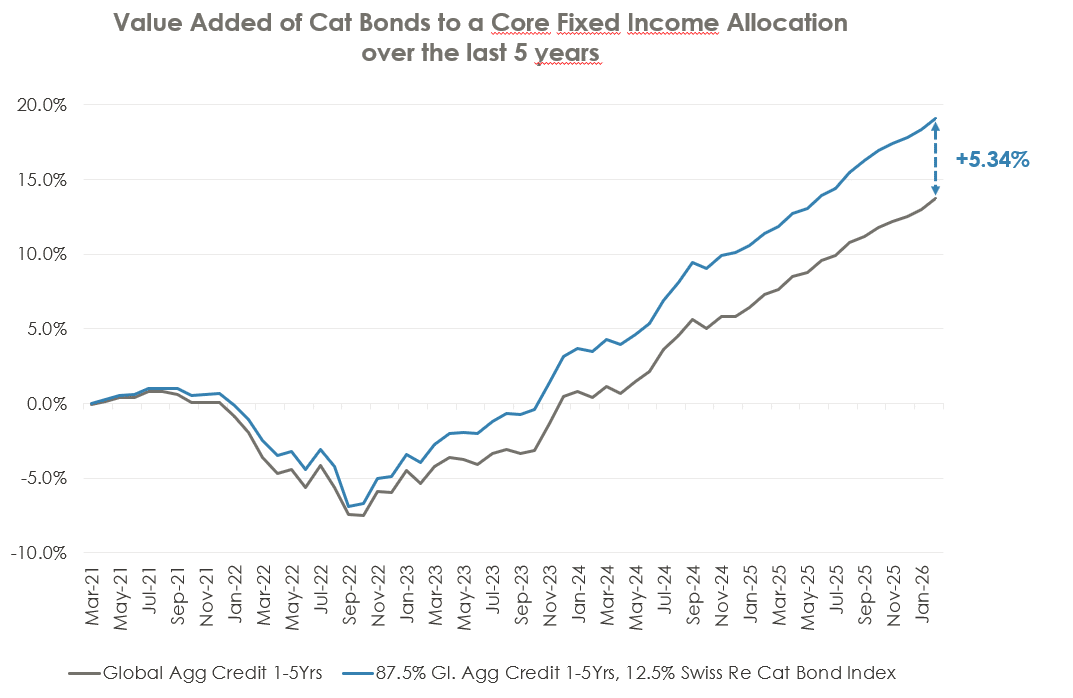

THE CASE FOR CAT BONDS AS A FIXED INCOME DIVERSIFIER

What are cat bonds?

Cat bonds (short for catastrophe bonds) are fixed income instruments used to transfer risks related to natural catastrophes from reinsurance companies to capital markets. As part of the broader insurance-linked securities (ILS) universe, cat bonds allow investors to access returns driven by insurance premiums rather than traditional financial market risks.

How do cat bonds work?

Instead of being used for capex like for usual corporate bonds, the proceeds are placed in a collateral to be readily available to cover insured damage resulting from events such as a hurricane in Florida or earthquake in Japan. If such an event does not occur over the life of the bond (usually 3 years), the proceeds are returned to the investor with an annual coupon made of the collateral interests plus the spread linked to the perceived risk of insurance from the related natural catastrophe (in other words, the “insurance premium”). Because returns are linked to natural events rather than economic cycles, cat bonds tend to exhibit low correlation with equities and traditional credit markets.

Performance Comparison: Cat Bonds vs Investment Grade Credit

Over the past five years, a traditional fixed income allocation (excluding Cat bonds) would have returned a cumulated performance of 13.73%, or 2.60% in compound annual growth rate. This is using the Bloomberg Global Aggregate Credit 1-5 years index hedged in USD, which already in itself would have been a wise choice as it outperformed the more traditional Global Aggregate index, thanks to its shorter duration and higher carry.

However, introducing a 12.5% allocation to Cat Bonds (equivalent tto 5% within a 40% fixed income / 60% equity portfolio), would have increased cumulative returns to 19.07%, representing an additional 5.34% of outperformance. Annualized returns would have risen to 3.55%. Importantly, this excess return was achieved with similar volatility.

Why Cat Bonds Improve Risk-Adjusted Returns?

The key driver behind this improvement is diversification.

Because cat bonds are very much decorrelated from financial markets. In fact, the weekly correlation between cat bonds and the MSCI World over the last 5 years was just 0.14 vs 0.37 for the above-mentioned credit index. Even the correlation between the cat bonds and the investment grade credit index was only 0.17 during the same period. This helps explain why, in terms of risk-adjusted return, adding some cat bonds to a fixed income allocation would have been a good decision.

They provide exposure to an uncorrelated asset class, helping smooth portfolio volatility while maintaining attractive yield levels.

Are Cat Bonds Still Attractive Today?

Today, cat bonds continue to offer compelling fundamentals. They offer a yield to maturity of 7 to 8% with no duration and no credit exposure, although with different risks uncorrelated with financial markets. By contrast, the referenced investment grade index currently offers around 4.6% yield to maturity, with 2.7 years of duration and A- average credit quality.

From a technical perspective, the outlook also supports cat bonds. Over the next couple of years, we expect massive supply of debt in the investment grade universe as issuers like Oracle need to finance their enormous AI capex. With developed market governments also having to refinance ever growing fiscal deficits, it is unclear how much demand will be left to meet the new supply of investment grade debt corporate bonds. This expanding debt supply may pressure traditional credit markets, reinforcing the case for diversifying fixed income exposure with alternative sources of return such as catastrophe bonds.

Manager Selection matters

One word of caution: Cat bonds are a specialized and complex asset class. Manager selection is therefore critical. Investors should prioritize experienced managers with strong underwriting capabilities, proven track records, and sufficient agility to exploit opportunities in the developing secondary market of this approximately $65bn sector.

Written by Julien Baltzinger

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only.

NS Partners provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data, quotes, research notes or other financial instrument referred to in this document. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation.

Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors.

Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request.

© NS Partners Group

Article tagged by: