Quarterly Investment Review – Q4 2025

Quarterly Investment Review – Q4 2025

We’re seeing substantial asset inflation away from the dollar as people are looking for ways to effectively de-dollarise, or de-risk their portfolios vis-a-vis US sovereign risk.

Ken Griffin

‘‘The multiples of technology stocks should be quite a bit lower than the multiples of stocks like Coke and Gillette because we are subject to complete changes in the rules’’ Bill Gates in 1998

‘‘I’m willing to go bankrupt rather than lose this race’’

Larry Page, co-founder of Google

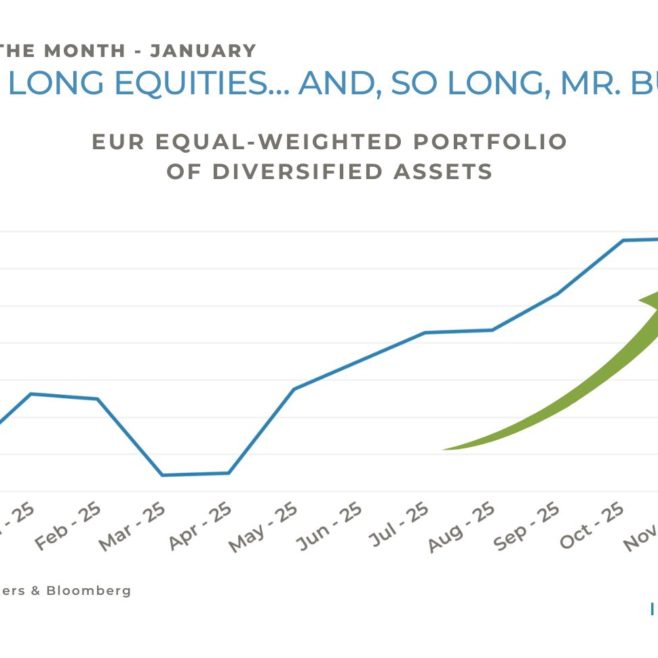

2025 was a gangbuster year for financial markets. Most equity markets delivered double digit gains, and most bond markets also generated positive returns. Apart from oil and the grains market, commodity markets were strong, and precious metals enjoyed spectacular returns. For once the US market was not the best performer. After a decade and a half of dominating equity returns the US produced one of the weaker performances, and if the currency is taken into consideration that result was even further behind, as the US dollar fell approximately 10% during the year. Elsewhere strong results were widespread across European, Asia and the Emerging Markets. The MSCI World Index was up 19.5% in US dollars or 16.9% measured in Local Currencies, and the S&P500 was up 16.4%.

Given the political background in 2025 this result might seem surprising. President Trump initiated a trade war by imposing tariffs which bludgeoned the world trade system. In Europe, the UK and France endured rolling political difficulties centred on both countries inability to contain their debt problems. The Ukraine war continues, while the Gaza war has reached an uneasy truce. What accounted for the market’s rise was good earnings growth in the US, while in Europe it was due more to a rerating. Underpinning all markets was an exceptionally supportive liquidity environment. Fiscal policies in all the major economies were benign – the US, China, Japan and most EU countries ran deficits of about 5% of GDP; low interest rates prevailed across the world; the US dollar weakened, which was particularly helpful for those Emerging Markets whose currencies were pegged to the dollar; and oil prices declined by close to 20% in US dollars and even more in other currencies, which has the effect of a giant tax cut for the world’s consumers. 2025 thus represented a rare occasion when the global economy, even though it wasn’t in recession, was stimulated by every lever at Governments’ disposal. This stimulus looks set to continue into 2026 as Trump’s One Big Beautiful Bill kicks in during January, as well as a promise of more deregulation. Germany’s giant fiscal boost will also get underway, and OPEC have increased their production to keep energy prices subdued. Given the midterm elections in the US in November President Trump will do everything he can to juice the economy in the run up to that.

Such stimulus could trigger inflation, and the biggest danger to stock markets would be a selloff in the bond markets, particularly the long end, on fears that the incontinent profligacy of government spending is unsustainable. While bond markets were stable in 2025, they have been poor investments in the last decade due to mounting concerns about Western debt profiles. According to Gavekal, since July 2020 the real return on a constant 10-year duration US Treasury bond has been minus 33%, and minus 37% for a German bund. Many Western countries debt to GDP ratios have risen above 100% and have annual deficits of 5–7% The interest cost on Government debt, for example, now exceed £110bn in the UK and $1 trillion in the US. As these debts spiral ever higher bond investors are being presented with the equivalent of investing in a share that yields 4% while it is annually increasing its share count by 7%. It was a striking feature of 2025 to see the complete failure of governments’ attempts to rein in these deficits. Trump campaigned a year ago on a promise to slash government spending, but Elon Musk’s DOGE effort collapsed in three months. The UK and France failed to remove even minor items of welfare spending from their budgets. It appears to be impossible to control the excesses in the public sector in these countries. In this context the change of Federal Reserve Chairmanship when Jerome Powell retires in May may be one of the most significant in history. The new Chairman will be chosen by President Trump on the basis that they will be expected to set rates significantly below current levels. Coming at a time when inflation is above target, deficits are at record levels, and global confidence in US policy is fragile, investors will have to grapple with how markets react to this new regime at the Fed. Meanwhile Governments will continue to overspend. The likelihood is that this spending will only be controlled when there is a failed bond auction which will force them to economise.

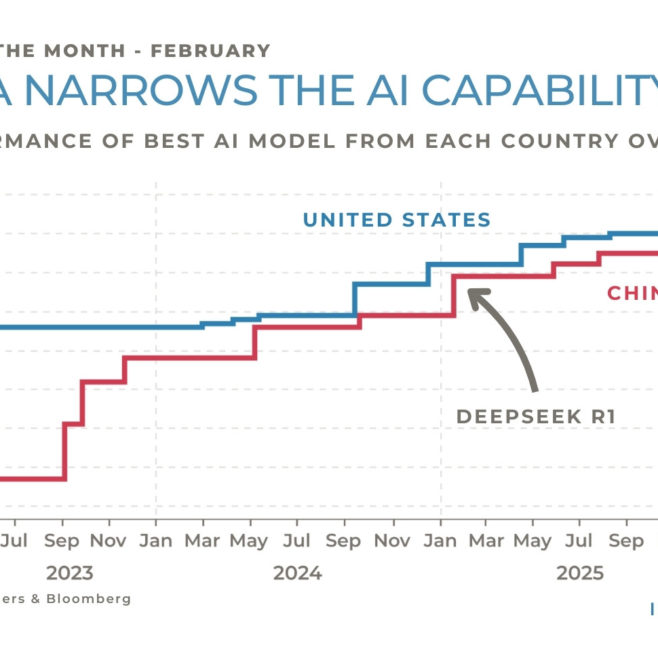

The US equity market’s superior returns have overwhelmingly stemmed from the extraordinary performance of its technology sector and particularly the largest companies, commonly referred to as the Mag 7. Since November 2022 when ChatGPT was released the US stock market has added $30 trillion in market capitalisation as the profits promised by AI (Artificial Intelligence) have come to obsess investors. As a result, the largest stock, Nvidia, has a larger weighting in the MSCI World Index than the entire Japanese market. In order not to fall behind in the AI race the leading companies are spending gigantic sums. Forecasts estimate that they will spend $566 billion in 2026, following $441 billion in 2025. Projections for the next several years suggest it will continue at these levels. Unlike the internet boom which rewarded successful operators for minimal capital investment, the AI build out is capital intensive and the returns uncertain. The datacentres that are at the heart of AI are subject to rapid obsolescence, with their useful economic life estimated at less than eight years. The relentless innovation in the sector could mean that whatever is cutting edge today is overtaken in the next few years leading to costly updates and overhauls, making it even more challenging to earn a satisfactory return on today’s investment. When money is allocated so fast in what remains a speculative industry the risks become much higher. There is little doubt that AI will be a transformational technology, but as with the railways and the internet much of the early capital invested may come to grief. The concern is that because the Mag 7 have been so entwined with the rise in the market if they fail to execute a satisfactory return on their enormous investments this failure will undermine the market. Their health has become the health of the entire market. Equally concerning is if this investment does justify itself then where will this profit come from? The most likely source is that it will derive from companies shedding labour. This uncertainty on how AI will be deployed into the economy means that firms have already reduced hiring, particularly of graduates. PwC have reduced graduate hirings by 35-40% for example. As firms work out how to use it, this jobs freeze may morph into firings. Historically when technology has made people redundant, they have found new jobs, but the speed of change this time may be quicker making the transition harder. Eventually the impact will be on the older generation who have less transferrable skills and the effect of this could be cataclysmic. This is likely to become an increasing political problem.

Click here to download the full document.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS Partners provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data, quotes, research notes or other financial instrument referred to in this document. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: