January general market comments

“Ballroom Blitz” – The Sweet, 1974

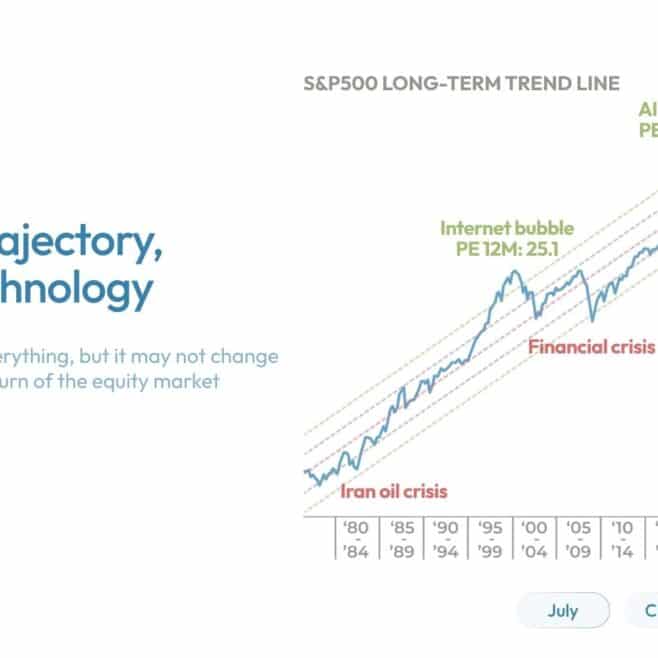

China’s announcement of its LLM tool DeepSeek has been felt like a massive blitz in the global AI ballroom in January 2025. Supposedly way cheaper and less resources consuming (semiconductors and power) than its US equivalents, the DeepSeek bombshell triggered a vast series of questioning about the – so far – winners in the AI space, from chips manufacturers to industrial companies offering data centers cooling and utilities, among others. This, added to the looming tariffs from the US administration towards many of its trading partners, has generated a lot of volatility in global markets, which have nevertheless shown surprising resilience in such a context. Earnings releases have probably helped equities in this environment: in most instances they were good, even if, in some cases, outlooks were less buoyant than expectations (but still showing solid growth in general). Perhaps the continued strength in Gold (+6.6% in USD) and Bitcoin (+9.0% in USD), unbeknownst almost all major currencies, should be an indication that there are some signs of nervousness among the investment community.

The MSCI World rose 3.5% in January, nicely helped, for once, by Europe (+6.3% for the Stoxx 600) which has outpaced the S&P 500 (+2.7%). Despite DeepSeek’s smash, the Chinese market was weak with a 3% fall for the CSI300, and more generally Value outperformed Growth (+4.4% versus +2.6%), the latter having painfully felt Nvidia’s 10.6% retreat. It is noticeable that among European markets, the defensive Swiss equity benchmark SMI was the star of the month with a 8.6% return, reversing part of 2024’s underperformance.On the fixed-income side, yields stayed mostly put, while Credit started the year with a nice show, as highlighted by the 1.25% increase for the Itraxx Crossover. Oil rose 1.1%, and the dollar lost some modest ground versus the Euro, the Yen and the Renminbi.

That’s it for this month’s Market Comments, stay tuned, markets never skip a beat.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS PARTNERS SA provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data or other financial instruments referred to in this general comment. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: