December 2025 Market Comments: Can the Bull Run “Do It Again”?

December 2025 Market Comments

“Do it again” – Steely Dan, 1972.

Investors would surely love financial markets to “Do it Again” in 2026; although Steely Dan’s classic is different as it’s all about repeating the same mistakes again and again, it would be nice to see almost everything rise in 2026 (barring Oil or Cryptos, it was hard to find a losing asset class in 2025). We’ve experienced almost every sentiment in 2025, from fear to greed, panic, FOMO, scepticism and euphoria; but, at the end of the year, bulls won.

So here we are, glasses raised at year-end, wondering: could the band play it one more time? Could 2026 be the encore — another year of liquidity, AI miracles, and soft landings? Or should we expect something different, in other words less capacity to overcome doubts when nasty events happen? “You go back, Jack, do it again, wheel turnin’ round and round”: we will face nasty events this year, like every year before; what matters is how do investors react to them. The market, like the crowd in the bar, is ready to dance again.

Just don’t ask what happens when the music stops.

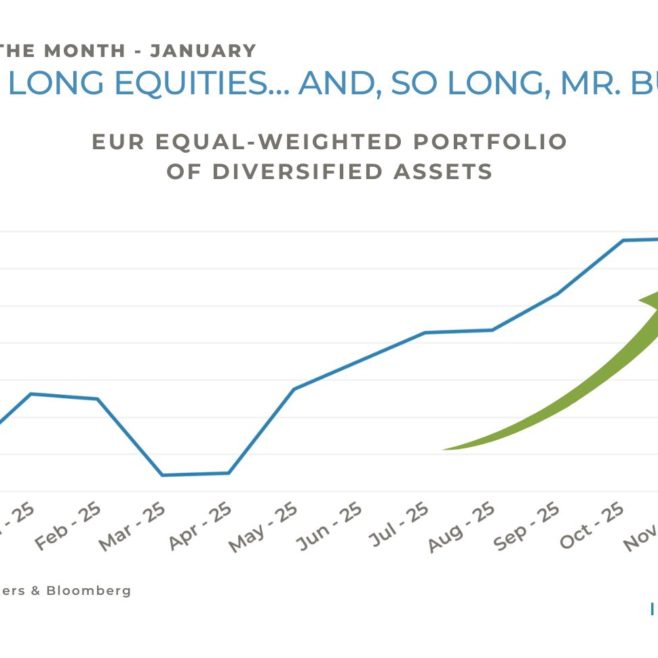

The MSCI World added 0.7% in December and closed 2025 with an enviable 19.5% gain; almost all equity markets posted solid double digit returns in local currency terms (S&P 500 +16.4%, Stoxx 600 +16.7%, Topix +22.4%, Emerging Markets +30.6%), with a more balanced picture between Growth and Value (+18.2% and +20.4% respectively).

The narrative around AI in general has been a major driver of equity performance, as well as the probable path towards a more dovish Fed, especially at the end of the year.

Currencies, and the dollar in particular, have been an important factor in 2025. The weak dollar (-13.4% versus the euro for the year) makes that returns, when measured in the same currency, are very different compared to local currency returns; for once, Europe has been the best performer in 2025 in this context.

Government bonds faced opposite fates; the US debt did well, while its German counterpart did not. Credit was strong, Oil extremely weak (-20% for the WTI) and Gold extremely strong (+64.6%).

We enter 2026 with a positive mood, but also many possible threats, like high valuations, poor public finances in many countries, geopolitical instability and a possibly shaky private debt situation. So please, Mr Market, “Do it Again” in terms of performances in 2026, but don’t “Do it Again” with complacency regarding valuations or leverage, we know this ends badly.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS PARTNERS SA provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data or other financial instruments referred to in this general comment. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: