In Pursuit Of Looking Sharpe

Many readers will remember the golden decade of hedge funds (the 1990s) that ended with the publication of “In Search of Alpha – Investing in Hedge Funds” the first of a series by the infamous Alexander Ineichen of UBS (a training manual for the latest incoming summer intern eager to learn about the mysteries of hedge funds) published a few months before the burst of the dot-com bubble in the year 2000.

Times have evolved since then, as changes in regulation have been a game-changer (Reg FD and the Volcker Rule to name a few). In addition, market participants have evolved due to the influx of institutional capital in the space and market dynamics have evolved as the average holding period of investments have become much shorter (thanks to increasing impact of the quants, artificial intelligence, geo-political events and Robinhood/Reddit platforms). The hedge fund investor base has also changed dramatically as Geneva, once the center of the world for hedge fund managers seeking capital from private banking HNW clients, has been overtaken by the largest pension, endowment and sovereign wealth funds which have taken the lion’s share of the industry.

Fast forward 10 years to the 2010s and you have the “lost decade” of hedge funds (proprietary desks disappeared, QE infinity made shorting very challenging and mutual funds / ETFs were in hindsight the obvious way to play the longest equity bull market in history). Will 2020 mark another golden decade for hedge funds? It certainly started nicely but proving to be less of a walk in the park so far this year!

Our dedicated absolute return mandate was launched 23 years ago using a multi-strategy approach and designed with the objective of generating consistent low volatility returns through periods of rain or shine, however it did face some difficulties during periods of black swan events like many of its peers. The FoF’s historical recipe for success had been in concentrating portfolios with the most talented single strategy managers in which you had the highest conviction. The downside of this approach is that you can become more volatile at times and before you realize one of your managers is down, it’s too late and it will take you a further 3 months to get out at best, or a year if not more (thanks to the infamous gate) together with the right to inherit a side pocket or two that will take 10 years to liquidate.

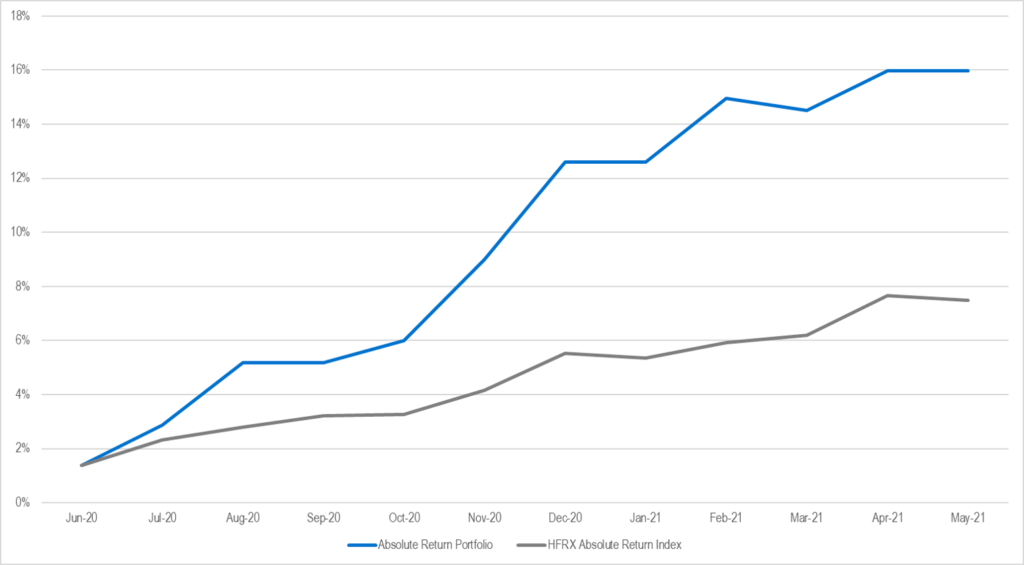

Twelve months ago, we wrote a piece entitled “Survival of the Fittest, a Darwinian Approach to Hedge Funds” which was to be the catalyst in undertaking a number of changes to significantly enhance the existing portfolio and make it more robust in market drawdowns and hence improve its Sharpe ratio (and Sortino). The result over the last 12 months have been promising as the Sharpe ratio generated has been 3.75 (which will probably never be repeated!) but more importantly the drawdown has been limited to 39 basis points with 4 of the last 6 months witnessing the worst alpha destruction in the equity space since records began. The changes have focused primarily on diversifying the portfolio across strategies, some of them being more niche and less scalable (therefore less accessible to pension funds/endowments) and having a risk management process based on the idea of the “electrified fence” whereby managers who reach their maximum drawdown limit will have their exposure taken down to zero and it’s “game over”. Add first loss capital arrangements and you take the concept of capital protection to the next level. Hence the multi-PM approach we described in our last piece which will enable us to limit drawdowns and compound returns over time increasingly outperforming the benchmark index over time. Our Multi-strategy and Equity Arbitrage allocations are complemented by what we consider some of the best managers in Credit Arbitrage and Discretionary Macro with a proprietary trading mentality in order to create a four-cylinder vehicle (ESG oblige). Most of our readers may have noticed the impressive comeback in discretionary macro managers in the last two years (a strategy Notz Stucki has been involved in over 50 years of investing in hedge funds and part of its DNA).

With the moves in the bond market together with the equity market’s shifts from growth to value as unpredictable as European weather of late, we hope to prove that our all-weather approach will have a better future as market volatility is here to stay. Let’s face it, what other alternative to fixed income do you have today?

Allow me to end this piece with a quote from Charles Darwin: “It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is the most adaptable to change.”

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only.

References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. Notz, Stucki provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data, quotes, research notes or other financial instrument referred to in this document.

This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the Notz Stucki Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer.

Additional information is available on request.

© Notz Stucki Group