Towards a slowdown in the US economy at the end of the year

Towards a slowdown in the US economy at the end of the year

At present, the US economy appears to be in good health: growth is approaching 2%, core and underlying inflation are falling, unemployment is low and oil and petrol prices are lower than this time last year. What’s more, corporate profits are starting to rise and artificial intelligence could lead to an unprecedented increase in productivity. However, there are some challenges on the horizon.

A few clouds in a blue sky

The Core PCE, the inflation indicator favoured by the Federal Reserve (FED), presents a major challenge. Despite a target of 2%, this index is still at a worrying level of 4.6%. In order to rectify the situation, the FED is considering raising rates one or two more times this year, which could hamper economic growth and investment.

Another potential slowing factor is the exhaustion of the surplus savings accumulated during and after the Covid-19 pandemic. According to several estimates, this surplus savings could dry up by the fourth quarter of 2023, considerably limiting the support that consumers provide to the economy.

Admittedly, after two disappointing seasons in 2020 and 2021, the tourism sector rebounded in 2022 and 2023 thanks to the desire of American families for holidays. However, this momentum is expected to run out around September-October this year, marking the end of the peak tourist season.

Another worrying phenomenon is the clear inversion of the US yield curve. Historically, this phenomenon has always been a precursor to recession or a period of virtually zero growth. Monetary policy, which operates with a certain time lag, could therefore begin to reflect this economic reality in the months ahead.

In addition, the US government is facing a substantial budget deficit, exceeding 5.5% by 2023. Maintaining this level of public spending is unsustainable for the country’s economy.

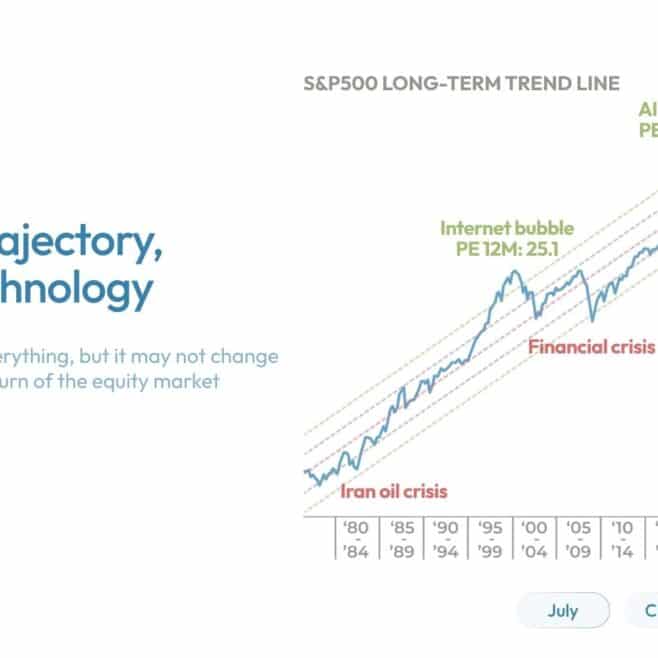

As a result, the valuation of the US stock market is starting to look a little high, at around 19 times projected earnings for 2024. However, investors do not seem to be worried about the economic situation.

A similar situation in Europe

Although we have mainly been talking about the US, similar observations can be made for the European economy, including the UK, except that company valuations in Europe are more moderate than in the US.

Given these factors, it seems likely that we will see a significant slowdown in the economy between now and the fourth quarter of 2023, which could go as far as a moderate recession or very weak growth of around 0.5%. Against this backdrop, defensive growth sectors (such as healthcare and staples), as well as quality investment bonds with maturities of 3 to 5 years, appear to be wise choices.

It’s a good time to take a break, just like the summer break we’re all taking.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of the date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS Partners provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data, quotes, research notes or other financial instruments referred to in this document. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the Finma cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: