May General Market Comments

May General Market Comments

“Steamy Windows”, 1989 – A tribute to the legendary and immortal Tina Turner.

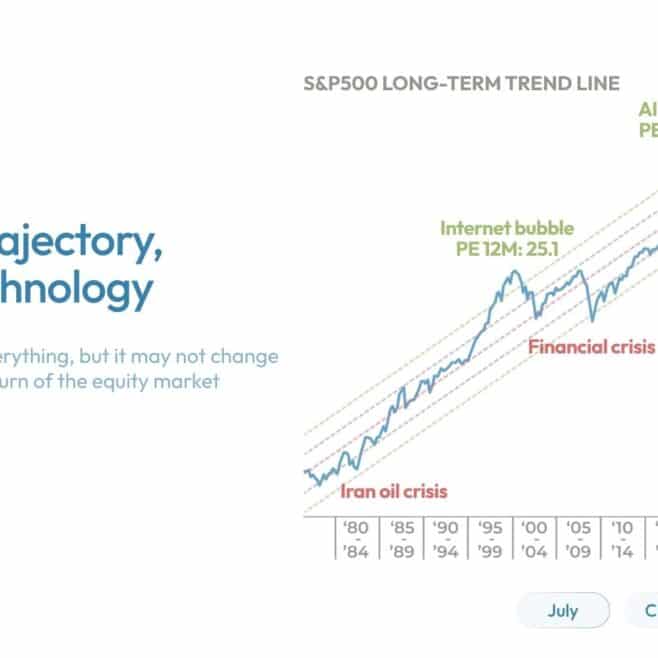

Trying to decipher the messages sent by economies and markets feels like trying to guess what lies behind steamy windows; you have an idea, but it’s not precise. Not more than 1 year ago, consensus was that a recession was inevitable in Europe and highly likely in the US, whereas it’s far less certain today; meanwhile, if not done yet, the Fed seems close to end its hiking cycle. China reopening should have triggered a massive boom for its equity market and commodities, but it hasn’t. Debt ceiling fuzz saw the dollar rise while the last minute deal, avoiding a default, has been followed by dollar weakness. Beyond an unclear short term horizon, two gigantic long term investment cycles still prevail: Digitalization and Cleaner Energy.

The crazy hype around AI and Nvidia shouldn’t make us lose sight of the fact that there will be profound consequences in terms of productivity with the widespread use of AI.

May 2023 was one of these very complicated months for equity investors who, if they were not exposed to the happy few rising stocks, had good reasons to be frustrated; the S&P 500 was almost flat, but it would have significantly been down without the contribution from mega-IT components who, besides the S&P, propelled the Nasdaq 100 7.6% higher. The absence of IT behemoths has cruelly been felt by Europe and Emerging Markets (down 3.2% and 1.9%), while Japan rose (+3.6%) with a weak JPY. Growth unsurprisingly humiliated Value (+2.3% vs -5.0%), while the strength of the dollar weighed on the MSCI World, which ended up the month down 1.3%.

Fixed-income was mixed: US 10 year yield rose 22 bps, Germany was stable and Italy, a good gauge of risk aversion, saw its 10 year benchmark yield fall by 9 bps. Credit enjoyed another very good month (+0.7% for the Itraxx Crossover), while all commodities plummeted: Oil down 11.3%, Gold down 1.4% and the broad CRB Index down 5,3%.

That’s it for this month’s Market Comments, stay tuned, markets never skip a beat.

Past performance is not indicative of future results. The views, strategies and financial instruments described in this document may not be suitable for all investors. Opinions expressed are current opinions as of date(s) appearing in this material only. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only. NS PARTNERS SA provides no warranty and makes no representation of any kind whatsoever regarding the accuracy and completeness of any data, including financial market data or other financial instruments referred to in this general comment. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. Any reference in this document to specific securities and issuers are for illustrative purposes only, and should not be interpreted as recommendations to purchase or sell those securities. References in this document to investment funds that have not been registered with the FINMA cannot be distributed in or from Switzerland except to certain categories of eligible investors. Some of the entities of the NS Partners Group or its clients may hold a position in the financial instruments of any issuer discussed herein, or act as advisor to any such issuer. Additional information is available on request. © NS Partners Group

Article tagged by: